Gill Capital Partners June 2022 Update

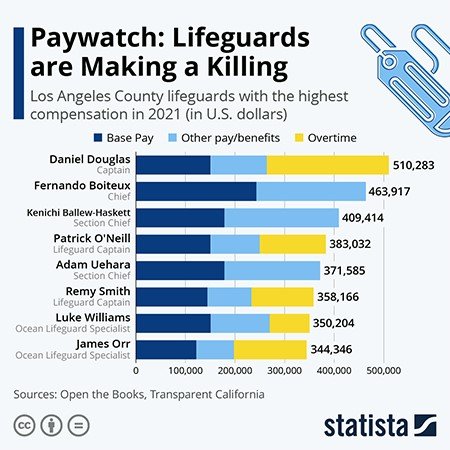

Summer is in full swing, and we hope there are fun summer plans in your future. Hopefully, high prices won’t get in the way of that planned trip or BBQ. There is plenty going on in the world of economics and financial markets, including another hot read on inflation, a renewed focus on interest rates, and the upcoming Federal Reserve meeting. We will get into all of that and more, but first, the interesting, maybe even ridiculous, data point for the month… Lifeguard salaries in California have people reconsidering their career paths.

Inflation, Inflation, Inflation

We received the monthly read on inflation this week, which came in a bit hotter than hoped. Consumer prices in May were up 8.6% compared to one year ago. The so-called “core price” index, which excludes volatile categories like food and energy, increased by 6% in May, down from the 6.2% increase seen in April. On a monthly basis, the CPI number jumped by 1%, with core prices increasing by 0.6% for the month. Some were hoping we would start to see inflation recede in May, but that did not occur. May’s increase was primarily driven by a sharp rise in energy prices, which rose nearly 35% from a year earlier, and groceries, which jumped nearly 12%. While food and energy prices are particularly impactful, inflationary pressures were broad-based.

Our view – This was not the data that the market was hoping to get. The market was hoping to see signs that inflation was beginning to roll over in May. Looking at the details, there is no way to sugarcoat this data. The inflation numbers were ugly, and this will continue to put pressure on the Fed to remain aggressive in its quest to rein in inflation. The last couple of months has represented a perfect storm for inflation. Everything from implications of the Russian invasion of Ukraine, Chinese lockdowns, heightened appetite for travel, and an unusually tight labor market. Other exogenous inflation pressures include factors such as diseases affecting livestock and continued supply chain disruptions. Furthermore, higher mortgage rates are already tightening real estate conditions. We remain particularly concerned about high energy costs as they continue to move in the wrong direction (from a consumer’s perspective), and extended time spent at these elevated levels is particularly damaging to consumers and the economy. We anticipate some level of demand destruction to begin occurring at these levels. Consumers will drive the quickening pace of switching to more energy-efficient products, such as electric vehicles, where the demand is already years ahead of the supply for many producers. We see glimmers of hope on the horizon, as the backlog in cargo ships waiting to unload fell for the fourth straight month in May, and inventories for many products are building, which will lead retailers to begin cutting prices to unload goods.

While the inflation number is ugly, we continue to believe that the pace of inflation will slow by year-end, as we have seen many times throughout history. As the old economist saying goes “the cure for high prices, is high prices”. Unfortunately, that generally leads to slowing economic conditions as well. The big question remains, will the Federal Reserve be able to thread the needle and bring inflation down while also landing the economy safely. We will see.

Interest Rates & The Federal Reserve

Interest rates have been moving higher again over the past week, given the inflationary picture. The market has already priced into current interest rates that the Federal Reserve will increase the Fed Funds rate from today’s rate of roughly 0.75% to roughly 3% in 2 years. The Federal Reserve is widely expected to raise interest rates by 0.50% at its next meeting on June 15th.

Our view – We remain skeptical that the Federal Reserve will actually increase rates as much as the market thinks over the next 2 years. Still, for now, the market already has this fairly aggressive positioning priced in. We very well may be in “peak Fed hawkishness” right now. Remember, the Fed has barely started raising rates, but the market has already priced in where they hope to get to in a couple of years. The economy adjusts rapidly now, much faster than it used to. Economic conditions have tightened, businesses are adjusting guidance, and consumers are adapting behaviors quickly. Markets are stuck in the upper half of the feedback loop, as depicted in the graphic below. However, the hint of slower inflation and/or the Federal Reserve looking to take their foot off the gas pedal will quickly kick markets into the lower half of the chart below and likely lead to significant gains for both stocks and bonds.

Market Update & Historical Perspective

Equity markets continue to flirt with the lows for the year, with the S&P 500 down nearly 20% from the beginning of 2022. Investors remain on edge as high inflation, the withdrawal of fiscal stimulus, and the heightened geopolitical uncertainty have created a challenging environment for global economies and financial markets in a very short period of time. Yes, market conditions have changed dramatically, and while the deck seems to be stacked against markets here, we like to remind investors of a couple of important considerations. First, the markets have already priced in a significant amount of bad news. Not to say that markets cannot go lower, they can, but a lot of bad information has already been priced into this market. Secondly, we think it is important to remember that in every business cycle downturn, equity markets lead the economy by several months, if not longer. In other words, equity markets typically bottom and begin to rebound even as economic conditions worsen. In each of the previous six business cycle downturns, equity markets bottomed a few months before economic data did. We know this type of market environment is unsettling and we believe investors should prepare themselves for continued volatility in the months ahead. Selling now following the declines that have already taken place with the hope of buying back at lower levels presents a precarious, if not near impossible task that would require perfect timing, lots of luck, and the possibility of having to buy back at higher prices. Historically speaking, the type of volatility we have seen combined with the negative sentiment readings tells us that we are closer to the end of the decline than the beginning.

As always, please let us know if you have any question or concerns, or if we can provide assistance with any other financial planning matters including education, taxes, insurance or estate needs.